What was once a promised staple of the Australian dream is now in jeopardy for anyone currently under the age of thirty. The numbers don’t lie. The numbers are alarming and stark. Retirement is slipping out of reach. The age pension is thirty thousand dollars a year, barely covering even the basic bills. At this rate, many Australians may not be able to afford retirement before they pass away. The age people can afford to retire is about to outpace our average lifespan.

In 2004 the average age to retire was just 56 years old, even younger if you were a woman. That is nearly a decade earlier than it is today. For someone who started working between 18 and 20, that meant roughly 36 years in the workforce. Today, the average retirement age has risen to 65, and even later for men. That’s a whopping 48 years in the workforce. The length of the average career has stretched significantly.

Superannuation was designed to support Australians in retirement, yet people are retiring later than ever. A lack of education and awareness about superannuation means most retirees still rely on the age pension as their main source of income. Many Australians only start paying attention to their super when it’s too late to make a difference. Historically, women have retired earlier than men, but even that trend is shifting as women now retire later than ever.

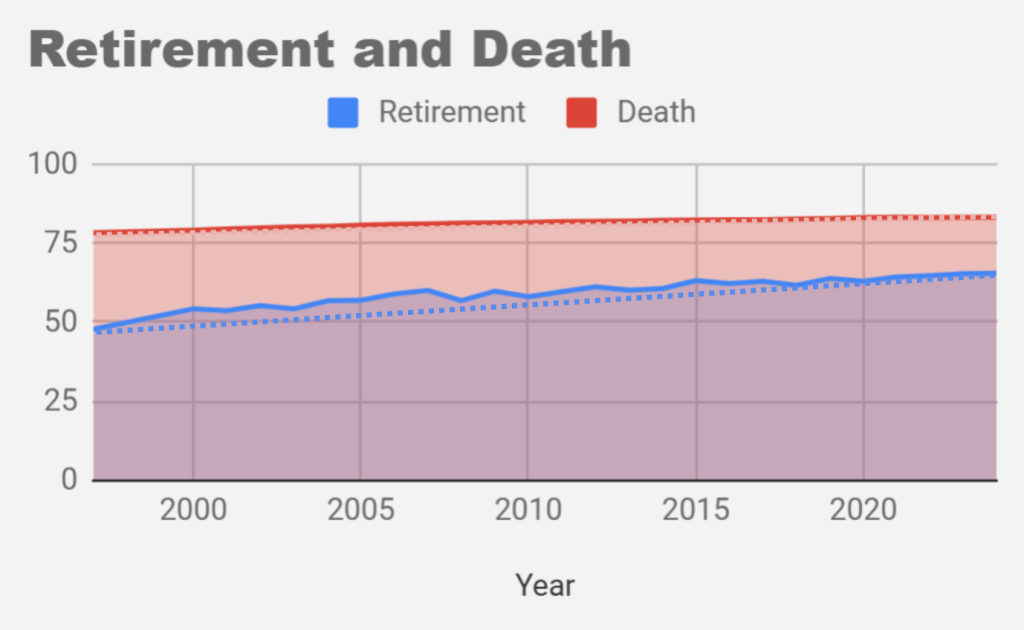

The retirement age is rising faster than life expectancy. If these trends stay consistent the average age to retire will be older than the average lifespan for Australians. At this rate, more people will die while still employed rather than ever reaching retirement.

All things staying consistent, retirement age outpaces average age of death in roughly twenty five years. That is to say, you will die before you hit retirement age. Without some form of change, Australians will be worked to death. This might sound extreme, but consider this, In 1997, Australians retired at just 48 years old. Today, most don’t retire until their later 60s. If this pattern holds, the average retirement age will push into the late 80s or early 90s, well beyond most people’s life expectancy. Barring some unbelievable jump in medicine, the average lifespan will not grow as fast.

When we dive into the numbers, large mortgages are mostly to blame for this worrying trend. As house prices climb, mortgage debt has ballooned, stretching repayment timelines while Aussie wages have lagged behind. Of course large mortgages come with large deposits. People are taking out their first mortgage later than ever. Delaying homeownership means delaying the final mortgage payment, which often delays retirement. Unfortunately that means that people stay working for longer. For perspective, both sets of my grandparents owned their homes outright before most people today even qualify for a mortgage. Their mortgage was also faster to pay off once they had one because wages were higher relative to house prices.

The Silent Generation (now mostly in their 80s and older) had to retire without superannuation, relying entirely on the age pension. By contrast, their children who benefited from the introduction of superannuation in 1992 have spent about half their working lives saving for retirement. They’ve witnessed their parents struggle to cover basic expenses on the meager age pension. Seeing the financial insecurity of their parents, many now fear retiring without enough super to sustain them. As a result, many keep working, knowing the age pension isn’t enough and that their super falls far short of what they need.

Retirement isn’t just about finances, it’s also about maintaining social connections. Families have become smaller over the years, many people approaching retirement are finding themselves more isolated. When polled, those close to retirement age listed social isolation as their second highest concern when considering retirement. Our communities aren’t as strong as they once were. They are far less connected than in the past. Many people don’t even know their neighbours’ names anymore. More people are staying in their jobs longer, at least partly for the social interactions it offers.

The death of retirement has had some major effects on our society as a whole. Besides the obvious decline in quality of life, as people spend less time in leisure during retirement, this shift has impacted so much of our everyday lives. Social, economic and career upheaval, all as a result of people working far longer.

The delay in retirement has made career progression slower within companies. This slowdown in career advancement has also contributed to a decline in company loyalty. Top jobs are usually occupied by those with the most experience, typically older employees who have had more time to accumulate it. In past generations, these older employees would retire well before age 60, allowing younger workers to move up the ladder.Now, with people retiring much later, they’re unlikely to give up their high-paying jobs to make room for younger employees. Older generations often complain that younger employees lack company loyalty. Why would they have any loyalty? The corporate ladder is clogged because top positions aren’t being vacated by retiring employees.

So the career paths of young workers are narrowed. As a result, the career paths of young workers are increasingly limited. There is a traffic jam at the top of the corporate ladder. Compared to retirees in the 1990s, older workers are staying in their jobs nearly twenty years longer. For younger workers, the only way to advance is often by changing companies when possible. The days of staying with one company for an entire career are long gone. The death of retirement killed any upward career movement.

From an economic perspective it isn’t all doom and gloom. The longer someone works, the better it is for the government. The government invests in education and collects taxes on workers’ income, which benefits the economy. In general, a skilled workforce will earn more. This makes education an increasingly valuable investment for the government, as people now spend more years contributing taxes. This means that educating someone has become a better and better investment for the government. Modern workers contribute significantly more in taxes than those from the 1980s due to their higher wages and longer careers. Furthermore, the longer people work, the longer they contribute to production. Increased production leads to greater economic growth for the country as a whole. Today, the economy benefits from nearly fifty years of production from a modern worker.

Finally there has been a significant social impact of people working longer. Grandparents are no longer retired by the time their grandchildren are born. In previous generations grandparents typically played a much larger role in raising their grandchildren, often providing regular childcare and support. The rise of the childcare industry can, in part, be attributed to grandparents working longer, reducing their availability to care for grandchildren. In the past, it was common for grandparents to help care for children aged zero to five while parents worked. They also played a significant role in the school run for children aged five to twelve. Now, as their grandchildren grow up, they’re still stuck in an office cubicle.

Perhaps the true cost of the death of retirement is the loss of the leisure time that many hoped for in their later years. After decades of hard work, nothing. There will be no time for the travel and family milestones that many envision in their retirement. There will be no traveling later in life. There will be no grandparents day at schools. Why? Because retirement is on death’s door.

Leave a comment